It would be easy to argue that a successful democratic government requires an educated and informed electorate. Such may still exist in America, though the popularity of Fox News sometimes leads me to think otherwise.

Here for your education is one of the best and most layman friendly explanations of the relationship between the US and China over trade and debt. It is used here with attribution, though not explicit permission from the January/February 2008 issue of The Atlantic, and was written by James Fallows.

Here's a tidbit:

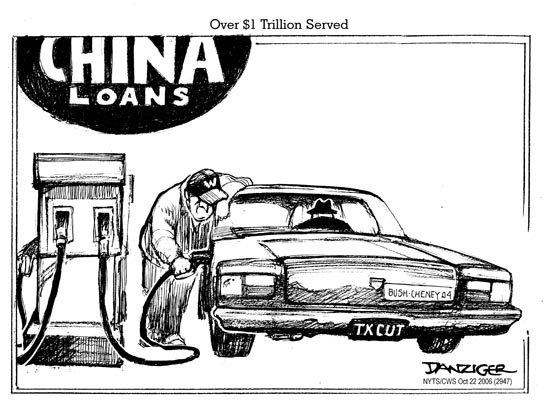

The $1.4 Trillion Question

The voyage of a dollar

Let’s say you buy an Oral-B electric toothbrush for $30 at a CVS in the United States. I choose this example because I’ve seen a factory in China that probably made the toothbrush. Most of that $30 stays in America, with CVS, the distributors, and Oral-B itself. Eventually $3 or so—an average percentage for small consumer goods—makes its way back to southern China.

When the factory originally placed its bid for Oral-B’s business, it stated the price in dollars: X million toothbrushes for Y dollars each. But the Chinese manufacturer can’t use the dollars directly. It needs RMB—to pay the workers their 1,200-RMB ($160) monthly salary, to buy supplies from other factories in China, to pay its taxes. So it takes the dollars to the local commercial bank—let’s say the Shenzhen Development Bank. After showing receipts or waybills to prove that it earned the dollars in genuine trade, not as speculative inflow, the factory trades them for RMB.

This is where the first controls kick in. In other major countries, the counterparts to the Shenzhen Development Bank can decide for themselves what to do with the dollars they take in. Trade them for euros or yen on the foreign-exchange market? Invest them directly in America? Issue dollar loans? Whatever they think will bring the highest return. But under China’s “surrender requirements,” Chinese banks can’t do those things. They must treat the dollars, in effect, as contraband, and turn most or all of them (instructions vary from time to time) over to China’s equivalent of the Federal Reserve Bank, the People’s Bank of China, for RMB at whatever is the official rate of exchange.

With thousands of transactions per day, the dollars pile up like crazy at the PBOC. More precisely, by more than a billion dollars per day. They pile up even faster than the trade surplus with America would indicate, because customers in many other countries settle their accounts in dollars, too.

The PBOC must do something with that money, and current Chinese doctrine allows it only one option: to give the dollars to another arm of the central government, the State Administration for Foreign Exchange. It is then SAFE’s job to figure out where to park the dollars for the best return: so much in U.S. stocks, so much shifted to euros, and the great majority left in the boring safety of U.S. Treasury notes.

And thus our dollar comes back home. Spent at CVS, passed to Oral-B, paid to the factory in southern China, traded for RMB at the Shenzhen bank, “surrendered” to the PBOC, passed to SAFE for investment, and then bid at auction for Treasury notes, it is ready to be reinjected into the U.S. money supply and spent again—ideally on Chinese-made goods.

At no point did an ordinary Chinese person decide to send so much money to America. In fact, at no point was most of this money at his or her disposal at all. These are in effect enforced savings, which are the result of the two huge and fundamental choices made by the central government.

[snip] Very interesting, no? Read the rest here. It is very worth the time, and will make you more interesting on the bar/cocktail circuit.

3 comments:

Very interesting.

Yikes indeed.

Thanks for this post and the article reference - very informative

Now I want to know more about "America’s crucial space sensors"...wha?

WOW. Speak of inevitability, here is the last paragraph of an incredible and disturbing article:

"Years ago, the Chinese might have averted today’s pressures by choosing a slower and more balanced approach to growth. If they had it to do over again, I suspect they would in fact choose just the same path—they have gained so much, including the assets they can use to do what they have left undone, whenever the government chooses to spend them. The same is not true, I suspect, for the United States, which might have chosen a very different path: less reliance on China’s subsidies, more reliance on paying as we go. But it’s a little late for those thoughts now. What’s left is to prepare for what we find at the end of the path we have taken."

Thanks Jeff. No one who reads your rants can say I didn't know.

Now, I am going back to my Mandarin Grammar book.

Blessings to you!

Post a Comment